So You Want To Learn About Economics, Pt. II

Some more of the coolest papers I know

A bit over three months ago, I published my most popular post. I discussed 11 papers that I found really cool and exciting. Being not entirely immune to the influence of popularity, I have decided to do a sequel, both covering those which I overlooked, and with an eye toward bringing you to the frontier of economics. These are all papers which I found beautiful. They’re the best of the best. I hope you like them as much as I do.

Gordon Tullock, “Problems of Majority Voting” (1959)

Gordon Tullock, “The Welfare Cost of Tariffs, Monopolies, and Theft” (1967)

Ronald Coase, “Durability and Monopoly” (1972)

Paul Milgrom and Nancy Stokey, “Information, Trade, and Common Knowledge” (1982)

Paul Romer, “New Goods, Old Theory, and the Welfare Costs of Trade Restrictions” (1993)

Jeremy Bulow and Paul Klemperer, “Auctions Versus Negotiations” (1996)

Steven D. Levitt and Jack Porter, “How Dangerous are Drinking Drivers?” (2001)

Ted Miguel and Michael Kremer, “Worms” (2004)

Matthew Gentzkow and Jesse Shapiro, “What Drives Media Slant?” (2010)

Marc Melitz and Daniel Trefler, “Gains from Trade when Firms Matter” (2012)

Raj Chetty and Nathaniel Hendren, “The Impacts of Neighborhoods on Intergenerational Mobility” (2015)

We begin with a few that I missed, and then proceed on to the edge of the field.

It is difficult for an individual to be irrational. In some views, it is impossible – humans are always maximizing their utility functions, and seeming irrationality is still optimal given their costs of acquiring information and so on. It is trivially easy, though, for groups of people to be irrational, and is indeed quite common.

First, it is obvious that if it is not permitted to trade favors, voting would take no account of the intensity of preferences. Ten people, voting purely selfishly, would vote no on allowing a building project on account of trivial inconveniences, while someone who would benefit immensely from building a home would be hurt considerably. Clearly, allowing for voters to trade favors improves outcomes.

However, this too has problems. Tullock has us consider 100 farmers who are voting on which roads to maintain. Every farmer has one road leading to their property, and for simplicity’s sake we shall say that they are the only beneficiary. Taxes are levied equally upon everyone. In an ideal world, each farmer would find the Kantian ideal of how much a road should be maintained, and vote to repair each road below the standard. Every farmer would profit, though, by always voting for their road and never voting for anyone else’s. If they did this, then no roads would ever be repaired.

Because they can trade votes and favors, they could organize into voting blocs, and agree to always repair each others roads, and disfavor the other groups. One could form a coalition of 51 voters, which levy taxes upon everyone to pay for their own roads to be repaired. Importantly, this coalition is not stable. Any group of 49 could induce 2 voters to break away from the ruling bloc. It’s not clear that the government will ever come to any decision at all!

James Buchanan would later comment (rather cleverly) that this instability of majority rule is, in fact, a good thing. If people expected to never be in the majority, ever, then they might withdraw from democratic government and rebel. It is precisely the weakness of majority coalitions which allows democracy to live. This paper also shows how we should be careful about what we put into the democratic domain. The repair of roads which only benefit one person is clearly something best left in the hands of private citizens, just as questions of which car to buy should be. But enough of what other people thought, we have another Tullock paper to talk about.

The Welfare Costs of Tariffs, Monopolies, and Theft:

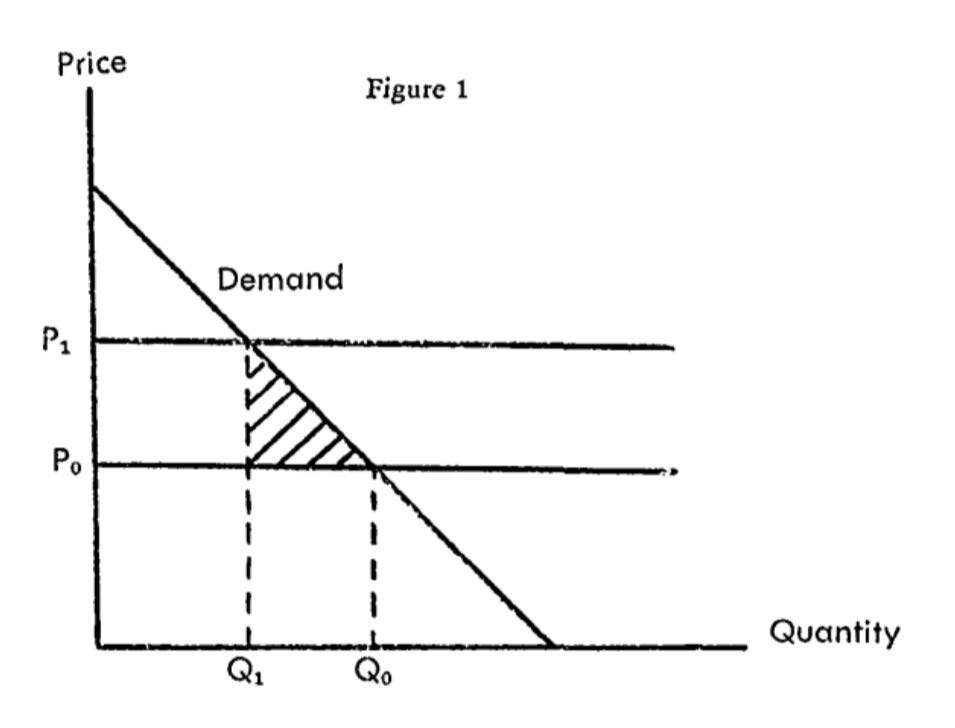

Monopolies, tariffs and theft all lead to a reduction in total output. We can see this in a simple diagram, as below. The price increases to P1, quantity produced shifts along the demand curve from Q0 to Q1, and the producer gains the rectangle between P0 and P1. The triangle is the loss to society from goods which would have been profitable to produce, but never are made.

The only trouble with economists’ story is that the losses are pretty small. Tullock’s argument is that the potential losses include not only the triangle of deadweight loss, but the entirety of the gains to the monopoly, or the protected industry. Competition happens in the political process too. If firms can profit by lobbying the government to protect them, then eventually the entirety of the surplus is gobbled up, and everyone is worse off. Likewise with theft. People will be willing to invest in guarding their property, up until the point where it becomes unprofitable. Meanwhile, someone embarking on a life of crime gives up other pursuits, which may have created something. We can avoid this by committing ourselves to never intervene in protecting some industries, no matter how they might call for it, or by punishing criminals sufficiently.

This is, by any standard, an unusual paper. It is a slight paper, just seven pages, of which two are simple diagrams, and unusually, cites no sources. Such are the things you can do when you edit the journal it’s published in! Yet, it has a profound insight. Imagine a monopolist selling perfectly durable good. Coase suggests all of the land on the United States. Further assume that each person demands one unit of land and no more, and that there is a downward sloping demand curve all the way down to zero. In order to maximize profits, the monopolist must necessarily not sell all of the land — the competitive price is where the demand curve hits marginal cost, or zero. So, the monopolist does this, and that is all.

But wait! There’s still land leftover. Whatever is he to do? Why, sell the land again, this time at a new, lower monopoly price; and so on until all the land is sold. The trouble is, everyone knows that the monopolist will do this, and everyone knowing this, they can simply wait until the monopolist drops his price to the competitive price. The monopolist is, in essence, in competition with future versions of themselves.

Unstated, of course, are considerable mathematical assumptions about future expectations. Stokey formalized it, and showed that the theorem — the “Coase Conjecture” — held under remarkably broad circumstances. Two equilibria are possible, as a later paper showed — this, and the so-called “Pac-man Equilibrium”, where the monopolist sets a price at the highest part of the demand curve, and promises never to lower it until someone buys, and continuing down the line until the entirety of consumer surplus is gobbled up, like Pac-man. Nevertheless, there is reason to think that, in large purchases, prices are constrained by being unable to bind oneself to the optimal course.

Note that I said for large purchases. There have been empirical tests of the hypothesis which have not found the stated effect, such as from Groseclose and Tabarrok (2023), who looked at the market for e-books. They found that prices remained persistently far above marginal costs (which they estimated by looking at the prices of books in the public domain). Of course, the median book on the market cost 49 cents, and it’s reasonable to think that people just aren’t paying as much attention to trivial costs.

Information, Trade and Common Knowledge:

Suppose that all traders in a stock market are risk averse, everyone shares a true prior about the world, and that everyone gets all the trades they want for hedging reasons done. We are now at equilibrium. Now suppose that a trader costlessly receives information which would lead to the expected return of one of the securities. For example, they might learn that there is frost expected in Florida, and that the price of frozen, concentrated orange juice will go up in the future. They are willing to bid above the equilibrium price for it. How many trades will occur? None! People will simply increase their listed prices so that no trades occur. The very act of offering a trade reveals information, and only a fool would take it.

This is why it is commonly known as the “no-trade theorem”. Trades do, of course, happen. But we must break one of the eminently reasonable assumptions, and setting out those conditions makes us think more clearly about what is going on. In this case, it really matters what we mean by “common knowledge”. There is no “ex ante” stage for us to reach equilibrium. We can never be sure that we are actually at equilibrium, or why someone is approaching us to make a trade. There generally exists mutual benefit for trades, and so long as people’s expectation of the gains from trade are high enough, markets can function. However, if this confidence is lost, then you can have a sudden and unexpected collapse of markets.

I found these slides by Stephen Morris quite clarifying in writing this section.

New Goods, Old Theory, and the Welfare Costs of Trade Restrictions:

This is the spiritual descendent of Tullock. The welfare costs of trade restrictions can be far larger than we might naively expect, once we allow for fixed costs and changes in the goods available. The graph in the commentary on Tullock is assuming that firms are not paying fixed costs, or that if they are, the tariff is unanticipated. Once that assumption is broken, some firms which would have produced at a loss do not produce at all, and the loss to the consumer is far greater.

That is only a small part of the contributions of the paper, though. What I found in it was an entirely new way of looking at economic growth. Most economic growth doesn’t consist of making old goods more efficiently, but in making entirely new goods, many of which have capabilities which did not exist in any form beforehand.

It is especially relevant now, as Trump prepares sweeping taxes on imported goods. Critics of the FDA write of an “invisible graveyard”, where those who die of medicines which could have been invented, but weren’t, go. The biggest costs of tariffs will be invisible too — goods which could have been invented, but never were. We are in some sense lucky that tariffs increase the cost of goods now, so that we are brought to our senses by paying more for everything.

Suppose the owner of a company wishes to sell it. If he is selling it to a single buyer, and the buyer has an unknown valuation drawn at random between two values (for convenience, 0 and 1), the optimal mechanism is to give the buyer a take it or leave it offer halfway through the distribution; if there are multiple buyers, then the optimal mechanism is to hold a second-price auction, with yourself bidding at .5. Alternatively, he could hold an open and fair second-price auction which maximizes social surplus. Suppose he could have the optimal mechanism with N buyers, or the fair auction with N+1 buyers. Which should he choose?

Surprisingly, the fair auction with N+1 buyers always produces more expected revenue than the unfair mechanism designed to maximize the consumer surplus. The revenue from a second price auction is given by N-1/N+1, so with two participants the expected revenue is ⅓. With one buyer, the optimal mechanism is to give a take-it-or-leave-it offer at .5, which is taken half the time, for an expected revenue of ¼. If you increase the N by one, then the expected revenue for the fair auction becomes ½, while the optimal mechanism revenue becomes 5/12. This is because it is as if there is a third participant — the seller — in the auction, and part of the time the seller ends up selling it to themself, and gaining nothing.

In a stylized way, this shows how the incentives of private actors can be aligned toward the good. Companies – efficient companies, at least – would prefer being able to sell to many, many people, rather than extracting as much revenue as they can out of a few. Expanding the market benefits everyone. Population growth also matters, for the same reasons.

How Dangerous Are Drinking Drivers:

We want to know how dangerous driving while drunk is. We can’t, however, simply use the fraction of drunk drivers involved in crashes without knowing what fraction of drivers on the road are drunk. Prior work used random road stops, but these suffered from a key flaw — without probable cause, the police can’t make you take a breathalyzer test. Even if they could, the external validity is questionable — the fraction of drunk drivers could vary over time.

Levitt and Porter come up with a strikingly clever solution. Grant that who drunk drivers crash into is effectively random. Then, we can compare the ratio of fatal crashes which involve drunk-drunk drivers, to those crashes which involve drunk-sober drivers and those which involve sober-sober drivers. If everyone were drunk, then all crashes would be drunk-drunk, and vice versa if everyone were sober. In between, the ratios can be used to find the proportions, because the likelihood of a drunk-drunk crash rises with the square of the number of drunk drivers, and the likelihood of a drunk-sober crash rises linearly.

Drunk driving is extremely dangerous. Drunk drivers are 13 times more likely to be involved in a fatal crash. It is, by far, the strongest predictor of causing a driving death, and imposes an externality in the order of 30 cents per mile (in 2001 dollars). It is also extremely common, with nearly 25% of drivers in the early morning hours being drunk. Thankfully, it did fall over the time period studied.

The results are all well and good, but I obviously did not include the paper for that. Rather, it is beautifully identified. Economics, to me, is at its best when it comes up with a clever but sound way to argue that one thing caused another.

I include this less for the study itself — though it is, of course, important, and its conclusions have largely held up — but as an opportunity to discuss a whole line of literature. The use of Randomized Controlled Trials (henceforth, RCTs) has revolutionized development economics, and has been a massive success. The use of RCTs has improved the lives of millions of people. We don’t need to rely on hand wavy speculation, or suspiciously identified quasi-experimental studies, when we can just go out and test whether our programs work or not. How do we best mitigate pollution? How can we improve health care in the developing world? Should we give people medical care or cash? Will a universal basic income pay for itself? These questions are fundamentally not answerable without field experiments.

It is true that RCTs have not, to my knowledge, led to sustained changes in the growth rate of economies. This complaint has always struck me as an isolated demand for rigor. Is it not always better to know what works and doesn’t work? More importantly, economic growth isn’t magical. It is the steady improvement of living standards. Raising the level which people live at, and doing it repeatedly, is economic growth itself.

Worms covers the effects of treating intestinal helminths, which infested a quarter of the world’s population. No one argues that one shouldn’t treat them, of course – the question is whether, in places where worms are endemic, we should simply give anti-helminth medication like ivermectin to everyone. This is not a question you can answer from pure speculation – we must estimate magnitudes. They, of course, find that the effects are strongly positive. People who received treatment attended more school, and later in life earned more income (as a followup study showed). Children who received the treatment work 17% more, are more likely to hold good jobs, and skip one fewer meal per week. They estimate an annual rate of return of 32%, which is insanely high.

These results were called into question, but the basic gist of the paper has held up. I suggest reading this blog post published on Givewell for more. Note that in finding deworming treatments to be worthwhile, Givewell discounts the expected benefits by 99%, and still found them worth funding for years. There is so much we can do in developing countries to improve the world, and it breaks my heart that we, America, are throwing away the little we do for the most selfish reasons imaginable.

Gains from Trade when Firms Matter:

The Journal of Economic Perspectives is one of my favorite journals. Its purpose is for authors to publish accessible versions of their work. In this, Melitz and Trefler cover the new revolution in trade theory – new new trade theory.

Explanations for trade start with comparative advantage. Countries are assumed to have identical production processes, and different in the resources they have. Countries have different endowments of land, labor, and capital, and they export the goods which require an abundance of the factors they have. This doesn’t do a very good job of explaining actually existing trade, however. Countries with similar endowments trade with each other, and what’s more, they tend to trade very similar goods with each other. Japan exports Hondas to the United States, and we export Fords to them. To explain this, Paul Krugman kicked off a revolution by focusing on increasing returns. Suppose there are two goods, both of which require a fixed cost to start producing, and constant marginal costs thereafter. Concretely, imagine a factory which must be built, before you can produce an arbitrary quantity of goods for the cost of materials and labor thereafter. If there are two countries/companies, it is obviously efficient for each country to only produce one good and trade with the other, thus minimizing

This did not fully explain the pattern of trade, as became apparent as we got better and better data. Firms are not identical to each other, but vary substantially. Markups (the difference between price and marginal cost) need not be constant over time, but can vary. What does this mean for the benefits of trade? In short, they get considerably larger. When we expand trade (or more generally, reduce transportation costs – work on trade liberalization can be applied without loss of generality to the coming of self-driving vehicles), we move the demand curve out (due to more people) while also making its slope shallower (because there’s more competition). The increase in market size benefits efficient firms more than the increase in competition hurts them, and vice versa for inefficient firms.

Newspapers are often biased toward one party or another. How much of this is due to the big businessmen who own the firms, and use it as an organ of propaganda? And how much is due to consumer demand?

In order to measure relative bias, Gentzkow and Shapiro must create a measure. Coding newspapers on a scale — 0-10, perhaps — is inadequate, because it isn’t continuous, and we can’t really say that going from 5 to 6 means the same as going from 9 to 10. They use the Congressional Record to find words which are used only by one party or another — “death tax” and “the war on terror” by the Republicans, “the estate tax” and “the war in Iraq” by the Democrats.

Now that they have a measure, they need to estimate demand. They take advantage of the very low marginal costs to serve all neighborhoods of a city, and compare the degree of slant to the circulation in different areas of a city with different political voting patterns. Places with a heavily Democratic vote-share tend to favor news slanted their way, and vice versa for Republicans. Having thus found the elasticity of demand slant, they scale it up to the whole city. Given the voting pattern of the city, what would the profit maximizing slant be?

The profit maximizing slant is very close to what people would demand. Therefore, consumers, not producers, are ultimately responsible for the proliferation of biased news. People like Rubert Murdoch aren’t imposing their views upon others; rather, they're simply providing people what they want.

I find this paper incredibly exciting for much of the same reasons I love Levitt and Porter’s paper. Using purely observational data, they are able to make a strong causal claim about a really important question.

The Impacts of Neighborhoods on Intergenerational Mobility:

The last paper in our collection is asking the third most important question in the world, behind only “how can poor countries grow” and “how can increase the rate of technological discovery”. In the developed world, how can we cost-effectively improve the lot of the poor? Are people held back by where they grew up? How would we benefit from encouraging poor people to move out of poor neighborhoods?

Experimental evidence is hard to come by here, although there has been some (see, for example, Chetty, Hendren and Katz (2016).) People generally do not move for plausibly exogenous reasons. They have three approaches, which can all be combined. First, they estimate the within family effects. If you move with three children, aged 8, 6, and 4, and they all leave the house when they are 18, then your children would have been in the area for 10, 12, and 14 years respectively. Presumably, each child is raised in a similar way, with the key difference being years in the area. The second is to find reasons why people move which are plausibly exogenous, or at least only a bit correlated with the outcome of interest. If hurricanes strike county X, but not county Y 30 miles away, then we can argue that people moving is due to the bad luck of where the hurricane hit and not any other reason. A similar logic can be applied to plant closures which are due to adverse demand shocks which affect the company as a whole. If Example Brand goes out of business because America just doesn’t demand Example Brand’s quality line of novelty Santa bobbleheads the way they used to, then the local plant closing is an exogenous shock. Finally, they look at variance in outcomes. If places have an effect on outcomes, then you would expect them to change the variance of outcomes to match the place that they move to.

Their key finding is that neighborhoods do indeed affect later earnings. These effects are linearly related to the time spent in that place, with later earnings converging by 3 to 4% per year of exposure to the place. There is no “key age” in early childhood when interventions must be done – it’s simply that younger children can get more time exposed to the better neighborhoods. At least 50% and as much as 70% of the variance in intergenerational mobility is due to area. 1/5th of the gap in earnings between blacks and whites are due to the county they grew up in.

All of this is made possible by the datasets they are working with being very, very large. Everything about this paper is big. It was so big it was split into two parts for publication, something I have literally never seen since Diamond-Mirrlees (1971) on optimal taxation. I think there’s a lot of good in the world which could be done if the US government collected more comprehensive data on its citizens, and made it easily available.