The Roman Market Economy

This was a fine book! He has a simple point to make, but makes it effectively: markets are really old, and the Roman economy was in fact a market economy which grew above the Malthusian equilibrium, primarily due to the increase in trade which was permitted by Roman peace and order. He writes very carefully, as he does not assume that it will be only economists reading. He explains clearly and precisely what is meant by comparative advantage or by a market; indeed, I was so struck by the perfection with which he demonstrated comparative advantage that I am going to turn to it whenever I teach the concept to anyone. I did, however, think it could do with some summarizing, and so I am writing this review on a chapter by chapter basis.

It bears mentioning that “The Roman Market Economy” is about six or seven papers in a trenchcoat, and as such, some of the papers which it is constructed out of will be linked to in this review. Uncited page number refer to the book itself, which can be found for free here.

Chapter one is the introduction to the book; he lays out the basic historical background of new institutional economics itself, and describes the plan for the book. He wishes to convince us that: economics is useful for studying history; that ancient Rome had a market economy; that the Pax Romana stimulated trade; that living standards improved generally; and that we are still learning about Roman history. A market economy, to Temin, is when there are enough market transactions where “many resources are allocated by prices that are free to move in response to changes in underlying conditions”, and so they move to equilibrium over time. (p. 6) An example of a non-market economy would be one where people are unable to move or exchange goods using prices, as in serfdom, or where prices and duties are driven by custom. He points to how nominal wages stayed the same for long stretches in early modern England, despite massive changes in conditions, like the price of wheat. (p. 8-9) He then shows how trade leads to improvement in welfare, in the example I spoke so highly of. I encourage you to read it through, but the simplified version is this. Imagine there are two production-possibility frontiers – the maximum which can be produced – for the two countries are reproduced here. On their own, they can consume along line A – but if they trade with each other, they can consume at any point along line B, a strict improvement.

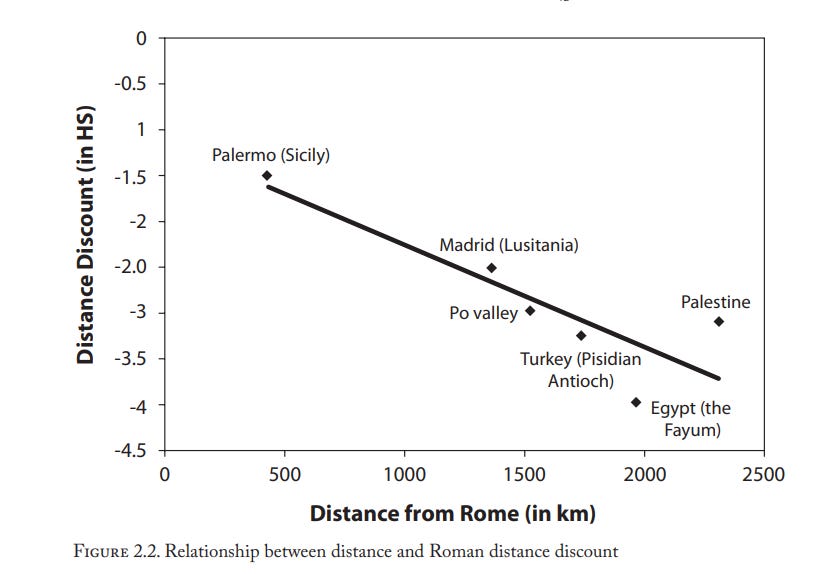

Chapter 2 is based on the paper A Market Economy in the Early Roman Empire. The goal is to show that the price of wheat was related to prices in other places, allowing for the cost of transit. If this is the case, then the markets are interconnected. The task of finding data for this is supremely difficult; the Romans, while members of all classes engaged in commerce, looked upon business as rather low-class, and as such we don’t have much written down of prices. We have very few observations of price data, spread over an extremely long time period. To clarify, Temin makes a basic assumption. Rome was the largest city (containing perhaps a million people) and was moreover the biggest demander of grain. The government handed out grain to nearly a quarter million people in Rome, in what was called the annona, and so we can assume that grain is always going to be valued in the provinces against what it would fetch in Rome. If it could be transported and then sold for a profit, then it would be. If cost of travel increases with distance, then the price should follow a regression line – and so it does.

You will note that there are only six observations – I did not exaggerate the difficulties of data collection! These span from 150 BC to 80 AD. However, inflation had not yet occurred (and would not occur until later in the Roman Empire), and we can check with statistical tests whether the relationship is likely to occur by chance. The regression is reproduced below.

He finds that it would be quite unlikely that this relationship would occur by chance. He then answers potential objections at considerable length, the most important of which being that the removal of a data point would substantially affect the result. This is true, but he replies “...choosing data points to make a result come out the way you want it makes the process circular; a statistical test only is possible when the data are chosen for reasons other than influencing the result of a test.” (p. 50)

The third chapter was developed out of “Price Behavior in Hellenistic Babylon”, and examines a fascinating data set. In Babylon the priests of the Temple of Marduk recorded astronomical data every day. They compiled these into clay tablets for each month, and included a price quotation of the cost of six major commodities: barley, dates, mustard, cress, sesame, and wool, given in the quantity available for a shekel of silver. This is a frankly incredible data set, far exceeding the quality and quantity of anything from the Romans, and can give us a window into prices in ancient economies.

He found that they behaved like a market economy – their price movement followed a random walk, and did not seem to have been determined by edict, as the prices varied relative to each other. (p. 57) A “random walk” is a feature of market prices; it is simply that it is impossible to predict whether the price today will be higher or lower, unless you know something others do not. Anyone who does know something will buy and sell accordingly, and so the price reflects the information available to all people. A price which didn’t vary is one set by edict, and would not be a market price. Temin also found that prices sharply increased in the chaos after Alexander died, presumably due to his successors debasing their currency to try and not lose control. This will become a recurring theme in the fourth chapter; economic policy is best when rulers have long time horizons, and are not incentivized to pawn the kingdom’s future.

Chapter 4 deals with inflation and political stability. He wishes to disentangle which caused which, or to show if there was a third variable which caused both. Because of the lack of price data, a detailed index is out of the question. Instead he codes inflation as either happening, or not happening. A measure of all prices in 301 AD is given by the Edict of Diocletian, which fixed prices for a large number of goods. A rate of average inflation can then be estimated form various price observations over time. Temin is very cautious in this section attributing causality – so much so that the chapter raises more question than answers. He points to the Antonine Plague of 165-180 AD as potential third factor which started inflation and political instability. In a plague, men die, but coins do not. People have more money relative to what is produced, and the price of everything goes up. The death estimates alone are inadequate to explain the scale of inflation even at the time, and so one would have to say that the plague started political instability leading to further inflation. However, isolating that as a cause doesn’t adequately explain why it stopped, and then restarted later. He cites another paper which gives a theory that the reforms of Aurelian in the 270s led to people using the silver weight in coins (which had been steadily declining a long time, down to being little more than bronze in a poor silver wash, according to this) rather than the face value. He cautions us against any one explanation (p. 90), and I think the main takeaway is to remember that inflation and political instability were invariably found together; the same lesson as the rise in Hellenistic Babylon.

Chapters five, six, seven, and eight all deal with the details of how roman markets worked. In chapter five, he shows the many ways which Roman merchants coped with adversity. The basic problem was a lack of information. A merchant who hires a man to sell grain in a distant port can not tell how effectively their agents are carrying out their wishes without some sort of adaptation. They also cannot guarantee that other people will pay them; facing this, a merchant might not send a shipment of grain until they have been prepaid for it.

The first level of contract enforcement was legal. State courts resolved disputes, and could issue fines in the case of fraud or breach of contract. Private judges were found too, who could act as arbiters in the case of disputes about private contracts. Merchants developed an extensive system of documentation (p. 106) which required multiple parties to attest to the quality and quantity of grain. A sample could be taken of the grain could be taken and shipped ahead, and the sample compared to the grain in the hold, to prevent the shipment being cut with inferior grains or even dirt. (p. 108) Permanent guilds of dock-workers allowed workers to sell a branded product, and monitor their fellow workers against theft. (p. 109-110) They could kick out anyone who stole goods, thus denying them employment in the field. The office of the Prefect (who was in charge of the grain distribution of Rome) helped to deal with lack of knowledge of prices by regularly publishing all information that was known, through the prices of public contracts (p. 105) and companies kept detailed records from their agents to estimate future prices themselves.

In chapter six he deals with the labor market, and with slavery in particular. He argues that slaves competed as part of the work force, and were not segmented into separate markets. Slavery in the Roman empire was of an entirely different character than the chattel slavery we are familiar with from the United States. Positive incentives were more important than negative incentives (p. 122) and perhaps half of all slaves could expect to be freed in their lifetime. Those who were freed faced no social stigma, as freed black slaves did; indeed, many would take so much pride in being freed (for it indicated rising on your own merit) that they would have it inscribed upon their tombstone. (p. 134). Education of slaves was normal, something unthinkable in America. There are even accounts of ambitious freemen selling themselves into slavery because it offered better prospects of advancement. Most slaves, however, were either born into slavery, or were abandoned children. Formerly they were mainly foreigners, but the pace of conquest slowed greatly after the Republic.

This is not to suggest that slaves were especially well off, or that they were not treated cruelly. Rather, the point is that their conditions did not sharply diverge from free workers, and that competition drew their wages toward an equilibrium with that of free workers. Temin considers it closer to apprenticeship, than to modern chattel slavery.

Chapter 7 discusses the market for land. There are three things which indicate, for Temin, a working market in land.

“First, there is a price for land that can change freely when conditions change. Second, people can buy and sell land at this price without reference to many outside authorities, that is, they can make their own decisions rather than reflecting the decisions of people not directly involved in the land sale. And third, there are few restrictions on or obligations from most landholdings and land transfers other than the payment of taxes.” (p. 140)

The first two are shown by papyrus records of land sales in Egypt. Prices changed, and they didn’t need to consult many outside authorities. (p. 140) He cites numerous literary sources describing sales and other business dealings. He also contrasts this with medieval Europe, where it was very difficult to sell land, there were heavy restrictions on what modifications could be done to them, and the institution of serfdom bound serfs to land for better or worse – they could not flee their master, but neither could they be evicted. Roman land markets were more flexible than that.

Chapter eight deals with how capital could be raised in the Roman empire. He compares this to how capital was raised in early modern Europe, and finds that, while not as advanced as England or the Netherlands, it was probably better than France before the Revolution. Borrowing between members of the elite on a personal basis was quite common (p. 168) and there was a trend toward writing these contracts down. These loans often did not require the transfer of physical cash, and could be accomplished solely by changes in ledger records. The legal maximum interest rate was 12% annually, or 1% monthly. The market was distorted by this price ceiling, but prevailing interest rates were often low enough to push the equilibrium interest rate below this. The law could also be evaded in the late republic by having a foreigner do it. (p. 170) A businessman looking for a loan could also turn to borrowing from the principle of an endowment left for some cause, or from a temple.

By the third century BC, de facto banks (called societates) formed, which lent commercially. (p. 172-173) These banks were recognized under the law, and while they had no formal legal personhood, courts devised workarounds to minimize inconvenience. These banks did quite a lot of business. This is supported by business records which were accidentally left behind in Pompeii as Vesuvius erupted; indeed, most of our knowledge of precisely how they operated comes from this. Local government would lend out idle funds as a matter of course, (P. 174) though the state itself rarely lent money (the only major loan the state made was to stave off the financial crisis of 33 AD), and there was no central bank. This meant that, unlike in early modern Britain with its Bank of England, nothing circulated broadly as a paper currency. The bills of credit given from person to person to represent a loan were limited in who would accept them.

Finally, businessmen could form partnerships financed through sale of shares. Cato, for example, “insisted that people who wished to obtain money from him form a large association, and when the association had fifty members, representing as many ships, he would take one share in the company”. (p. 188) The societates did not die with the death of an owner, and shares did trade at variable prices. This is not, as Temin sadly notes, something which we know as much about as the banks.

I mentioned the 12% annual limit on interest. This can be worked around, when inflation is low. The nominal interest rate is equal to the real interest rate plus the rate of inflation, and so when inflation skyrocketed in the later empire, the banks disappeared.

The final section is on measuring the economy as a whole. This is, needless to say, extremely difficult. Because there was no authority taking down the sort of statistics we can work with today, we must resort to some sort of proxy. Archaeology can give us evidence of consumption; pottery, for example, lasts for a very long time, and so the availability high quality, wheel-thrown pottery in excavations (so argues Ward-Perkins in the 2005 book “The Fall of Rome”) can stand in for economic conditions. In a similar vein, the number of shipwrecks, and the cargoes contained within, could tell us the amount of trade which went on. However, such proxies do not always indicate growth. Suppose the number of shipwrecks went down. Is that a sign of recession? Or did they simply get better at sailing ships? (p. 235) The problem with pottery is that it is not the only good sold; it is a reasonable indicator of incomes generally, but its availability could vary for reasons which affected the market for pottery alone. We could try and construct an index of goods produced, but this doesn’t tell us anything without population figures – another extreme difficulty. Remember that, above all else, the data is very thin. Measuring the sale prices of slaves, if we grant that they are in competition with the labor market generally, should indicate real wages, though this is complicated by the fact that people can be very different from each other, and we cannot measure this. Further, all attempts to measure things by prices are thrown into complete anarchy by the periods of inflation. Notwithstanding these immense difficulties, the rough contours of the Roman economy can be estimated. (Temin discusses the clarifying assumptions between pages 206 and 217 – if you are interested, I advise that you read the section online.)

In chapter ten, we must discuss the Malthusian trap. Assume that fertility is related to prosperity; that people have more children as they have better living standards. Assume too, that the gains which can be achieved by agriculture are not limitless, and further, that once all land is put under cultivation, it’s quite difficult to grow more food. Reproduced below is a graph of the Malthusian model, showing the effects of a plague. (p. 228)

The top graph are births and deaths (B and D). When the two equal each other, the population is stable. The model below is the amount of income a given population can have, where n* represent the population and y* the income. As you can see, a plague is an increase in deaths, and so the death curve shifts out. The number of people declines, but the income per worker goes up. Over time, the population of a country will expand to subsistence level, the minimum needed to survive. Any improvement in health or sanitation would actually make life otherwise worse, as more children will survive to eat up any surplus food; and a plague is extremely good for living standards, as it increases the ratio of land to men. This is borne out by the Black Death, which led to a large and long lasting rise in real British wages. The Antonine plague had similar effects, though naturally the data is much more limited.

The important point about the plagues is that fertility does not perfectly match prosperity; it takes quite a long while for it to catch up. As such, it really is possible for an ancient society, laboring under Malthusian constraints, to nevertheless have a sustained rise in income.

The final chapter is an overview of all the GDP estimates which have been made in the literature, showing their precise assumptions of annual consumption, prices, population and so forth. The most important thing I learned from this was to not take estimates of Roman GDP literally. The methods are, by necessity, so rough, that any specific figure has frightfully large error bars, and they’re nowhere near as precise as they sound. Temin’s personal estimate is that per capita GDP was equivalent to 1,000 Gheary-Khamis dollar (which is basically what a hypothetical dollar in 1990 could purchase), but he arrives at this by a rather circular assumption. He assumes that Roman Italy was in roughly the same position as the Netherlands in 1600, and then extrapolates from the percentage of income that Italy got to the whole of the empire. It implies that the income of the empire as a whole was similar to Europe in 1700. The best argument for this estimate is microeconomic, as he admits on the last page of the book; if we grant that they had similar institutions and trade, then they’ll probably be close to each other in income.

And so concludes my summary of “The Roman Market Economy”! I was convinced by the argument; Rome was (unquestionably to me) a market economy. It was also a salutary warning to take GDP estimates of ancient polities with a major grain of salt. There is just so much which is unknown and unmeasurable for us to be precise.

I have some general thoughts on the Roman republic and empire, about why it expanded to hegemonic status, and why no other empires followed it. Some are rather speculative, but I hope you will bear with me. First, Rome was more akin to a kingdom in an archipelago, than to a terrestrial government. The low cost of sea transport allowed it to more efficiently supply its troops, something which any potential empire in central Europe could not do. It depended on trade with Egypt for its grain, and I believe existed at just the right time climatically to take advantage of it. Egypt would later become desertified, and the weather would turn cold at the same time (the mid 200s) that the Roman empire began the long process of decomposition. Justinian and the other Byzantine kings were unable to restore the empire, in a large part because of the unfavorable climatic conditions. That is the first speculation, and I’d be glad if anyone could point me to the appropriate literature on long run climatic changes. That, and also the slow, iterative improvement of crops and livestock, are pet issues I think deserve more study.

The other reason is that maybe the Roman republic was just really weird. It is worth remembering that the territorial expansion of Rome stalled out under the empire. Some of this was because the territories with a high value to conquer were already conquered, but a lot of this is due to the incentives which emperors faced. Unlike the consuls, they had their whole reign to do what they wished; on the other hand, the consuls had a single year in which to make their name. This pushes toward a much higher pace of military activity. Further, the Roman conception of citizenship was unusually inclusive, and assimilated those whom they conquered. By working with groups, rather than coercively extracting resources, they were able to mobilize far more troops, and better troops who tended to want to be there, than their opponents. Where the Carthaginians had to rely on mercenaries, the Romans could simply call upon the people whom they conquered – who willingly responded. One could argue the late stages of the Roman collapse were due to the failure of the Romans to integrate the populations which in previous times they would have. Had the Goths not been treated so haughtily, or had they been dispersed when they were given land, Emperor Valens need not have been killed at the battle of Adrianople in 378 AD.

Perhaps I am mistaken in wondering why there wasn’t a new European hegemon. Rome may never have been particularly European, and the successors to their hegemony can be more properly thought of as the Byzantines, then the various Arab and Turkish caliphates.

As always, if you have any comments, criticisms, or links to related research, please tell me! Thanks.