What Do Unions Do?

Understanding the size and causes of the union wage premium

A union is a collusive cartel of workers. By bargaining as one unit, they are able to increase their bargaining power relative to bargaining individually, and raise their wages. In some circumstances, this will be inefficient, with the union commanding monopoly rents; in others, the bargaining power of the union will balance out the bargaining power of the company, raising employment and output. In either case, theory suggests the wages of unionized firms are higher. But by how much? Does this even hold in practice? And does doing this raise welfare?

Because there are reasons to believe that unionization will reduce wages for workers. In the United States, a firm becomes unionized when 50% or more of a workplace votes for it. The remaining workers are forced to be represented by the union, whether they like it or not. Since unions compress the payscale, such that better workers are paid less and worse workers are paid more, people could be voting for unions in order to redistribute from their coworkers to themselves. Employees might also vote for a union which will redistribute to them, at the cost of the company being more likely to go bankrupt long after they retire.

My best read of the evidence is that a union raises wages by around 7% for currently unionized employees. The wage gains from a redistribution of rents evenly across workers. Wage compression exists, but redistribution from worker to worker is only a small part. These are the current effects – unionizing more of the economy will have declining marginal returns, and will likely turn negative quickly — and take into account both the reduction of productivity by unions, which biases estimates up, and the spillovers to other firms’ wages, which biases estimates down.

I do not believe that unionization is efficient. While precise figures are lacking, it is unlikely to be a better method of supporting the poor or working class, both because union workers are not disproportionately poor, and also because their methods of extracting surplus are not restricted to just wages. I will note that while the best paper on the effects of unions on productivity finds a positive partial equilibrium effect, but that is only for some markets, does not benefit the consumer, and the aggregate effects are likely negative. I believe that unions reduce total welfare.

Understanding what the real effects of unions are is extremely difficult. Everything is endogenous, which will invalidate the basic exercises which we would have hoped were possible. Consider simply regressing wages on union membership. We will naturally need to control for things which might systematically vary with both income and union membership, like education and skills. Doing so gives you a premium of about 13-15% of wages. Firms which are unionized are also substantially more productive than those which are not. These controls are clearly insufficient, though – the decision to unionize is not a random one. Employees unionize precisely when the gains are expected to be largest, which will bias our estimates of the wage premium upwards. How do we get around this?

One appealing method is to use a regression-discontinuity approach at the 50% threshold for unionization. The idea is that a vote which passed by 51% is probably awful similar to a vote which failed with only 49% of the vote. Dinardo and Lee (2004) are the first to do this, and rather surprisingly find no effect on anything. There’s no increase in firm exit, no change in employment, and most surprisingly of all, no change in wages.

But this is also not good enough, for two reasons. The first is that the key assumption – that votes at 51% are awful similar to votes at 49% – does not actually hold in the data. Frandsen (2021) finds that close union elections get systematically tampered with depending on which party is in office, leading to close elections actually being substantially different in characteristics. The “tampering” which we’re talking about might be, for instance, waiting until after the election results are known to take up the argument that the “workplace” was improperly defined, and some votes should not be counted. This will make the firms which had a close election that passed substantially different from those whose vote just failed.

After correcting this, Frandsen finds that the wage effect is still zero. The firms, however, are badly affected. They employ fewer people, pay workers less, and are more likely to exit.

The other issue is more fundamental. With a regression discontinuity, you identify the local average treatment effect. You see what the gain to being unionized is, if your union is right on the threshold of being beneficial to workers. If the union were obviously promising to workers, then we would expect it to pass by a wide margin. We are going to badly underestimate the firm wage premium using only close elections. There is suggestive evidence for this in Lee and Mas (2012) – unionization reduces stock prices by much more when the union vote is won by a wide margin.

To get the average treatment effect, we use the Abowd-Kramarz-Margolis decomposition instead. This is the framework for modern labor economics, and you should understand what it is. Some workers, even after controlling for everything that you can see about them, are going to earn more. Likewise, some firms are going to pay more. In the cross-section, you cannot tell these apart. You don’t know whether high-paying firms are like that because they are high-paying firms, or because they simply attract higher paying workers.

So what you use are moves of workers from firm to firm. Worker Q moves from Firm A to Firm B, and his wage drops. You get a little bit of information indicating that Firm A is a higher paying firm than Firm B. In your data, which are administrative payroll or tax records, you observe millions of moves, enough to link together all of the firms. You estimate fixed effects, one for each worker and one for each firm, and that’s it.

An aside on matrix algebra. A fixed effect allows you to estimate a separate intercept for each person and each firm. How this works, concretely, is that you have a very large matrix Z. The rows are person-years, and the columns are equal to the number of workers and the number of firms. Each row has exactly two 1’s, ticking off which worker this is and in which firm they worked. Your formula for the slope is (Z’Z)^-1 times Z’y, where y is the outcome – wages – and Z’ is the transpose matrix. What we’re aiming for is the covariance of x and y, or how much they change together, divided by the variance of x. The first term takes Z multiplied by the transpose Z’ in order to make it invertible. (The matrix needs to be square and linearly independent to be invertible). Z’y is the covariance of Z with wages in logs. Multiplying by an inverted matrix is linear algebra’s way of dividing. The 1’s and 0’s for the fixed effects mean that you solve for the intercepts of just the group, but you get the slope from all of the observations together, at the bottom of the matrix, left over from multiplying.

This is too large to invert. We have tens of millions of workers, and hundreds of thousands of firms. So instead, we make use of the Frisch-Waugh-Lovell theorem, with a modification. With a single fixed effect per row, you can simply subtract the group’s average value, then wipe out the fixed effects. This is like sliding down every data point to be related to the origin. With two fixed effects, firm and worker, this does not neatly resolve in a single operation. However, we can reach the same result by iteratively subtracting the group mean of workers, then the group mean of firms, then back and forth until there is nothing more to subtract.

Now that you have the fixed effects, you can see how much variance goes away when you apply each one. How much variance disappears when you apply worker fixed effects? That’s how much of high pay is due to the unobserved characteristics of the workers. The variance that disappears when you apply firm fixed effects is the wage premium of high-paying firms. You’re also able to describe the sorting of high wage workers to high wage firms. To get the effect of the union, you look at what happens when workers change in and out of union jobs. You then subtract out the component which is attributable to unionized firms being more productive, and what remains is the union wage premium.

There are a few difficulties for these AKM estimates working. First, there must be no match-specific effects. The wage is simply the result of combining the firm wage premium and the worker wage premium (plus error). This wage premium must be portable from firm to firm. Second, workers moving from firm to firm has to be exogenous, and cannot be due to unobserved changes in skill. Third, what we are measuring is the variance explained. Since our sample is finite, noise will lead to us understating the percentage of variance explained. Fourth, specific to the union context, we are unable to account for the union’s possible effect on productivity. Only rarely do we observe a firm change union status, and when we do, we cannot exclude that the unionization decision was related to future prospects. If unions target productive firms, and then make them worse, we will misread the welfare consequences.

We have solutions for each of these. But perhaps it’s better to get to the papers, of which Beauregard, Lemieux, Messacar, and Saggio (2025) will be a seminal one. They have detailed data from Canada for the year 2001 through 2019, which contains every worker and every job. Dropping the firms for which we lack sufficient linkages and workers whose wages are not consistent with full time work, we are left with about 1 million firms and 17 million workers.

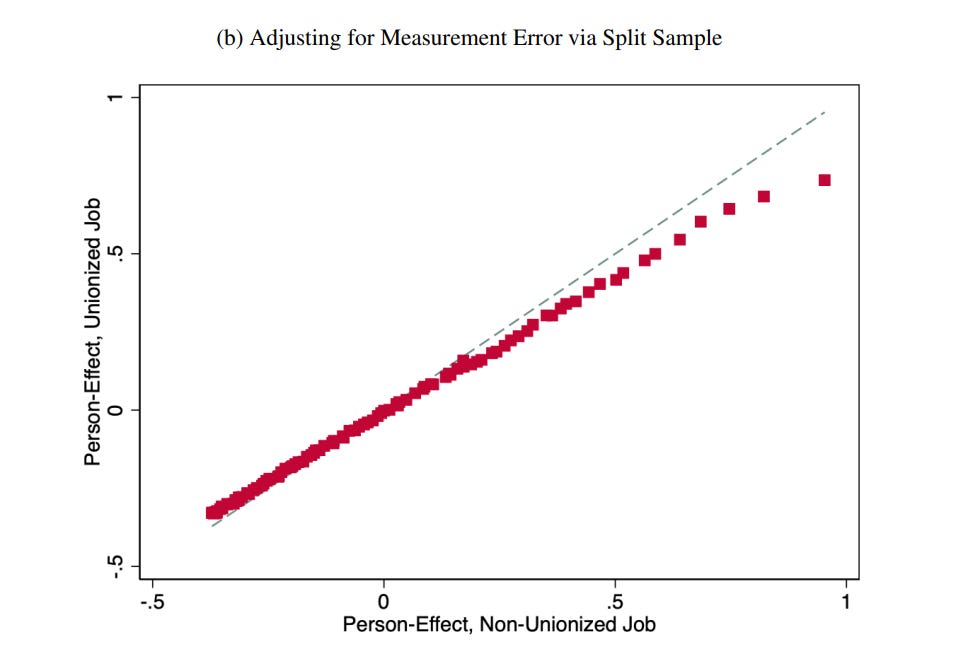

They find that unionized jobs pay 19 log points more in wages. Union workers are also more experienced, so conditional on observed worker characteristics, the premium is 15.5 log points. Unionized firms are then 28 log points more productive. Adjusting for this allows us to attribute 60% of the premium – 9 percentage points – to rent-extraction from the employer, and the remainder to unionized firms being more productive (without taking a stand on why they are more productive).

Unions not only raise the wages of workers, but they also compress them. Especially capable workers are less able to renegotiate their terms of employment. BLMS are able to capture this by allowing the worker fixed effect to vary depending on whether they are in a union or non-union job. 40% of the union sample switches back and forth between a union and non-union job at some point, allowing us to identify if the union premium systematically differs across workers, and the firm effects are identified from companies which hire both union and non-union labor. The remaining 60% of their sample is imputed by matching on everything we can observe about the workers, and assuming their union premiums would be the same.

After adjusting for wages at the first job, this looks less like redistribution from top to bottom, but a soft wage cap for the most skilled workers. This tracks with how the amount of rent extracted does not increase with productivity, but seems a one time amount distributed evenly across workers.

So how do they deal with the four challenges? The easy one to deal with is the limited sample bias. They follow best practices from Kline, Saggio, and Solvsten (2020), who show how to deal with bias by reestimating the equation leaving out each firm-worker pair (with a computational trick to avoid having to redo their work hundreds of millions of times). But more importantly, this doesn’t matter for estimating specifically the union wage premium. Sure, worker and firm effects explain too much, but both union and non-union jobs are biased the same. The difference is unaffected.

They allow for complementarity in a limited manner. The current gold standard for estimating complementarity in AKM models is Bonhomme-Lamadon-Manresa (2019), who bunch firms into groups with k-means clustering based on the distribution of wages, and then look at wage effects when workers move within a cluster of firms versus when they move across clusters of firms. BLMS only allow complementarity of people with union or non-union jobs, but they do not find substantial effects. They can take comfort, though, in how Bonhomme-Lamadon-Manresa estimate a minuscule change in aggregate variance explained from complementarities.

The big concern is that moves are not exogenous. It’s always been a bit hard for me, to be frank, to make economic sense of the exogenous job movements requirement. People are maximizing agents, and they don’t have to leave for a job that pays them less, if nothing has changed. Imagine people are searching for jobs while on the job. They will naturally only leave if their wage is better than before!

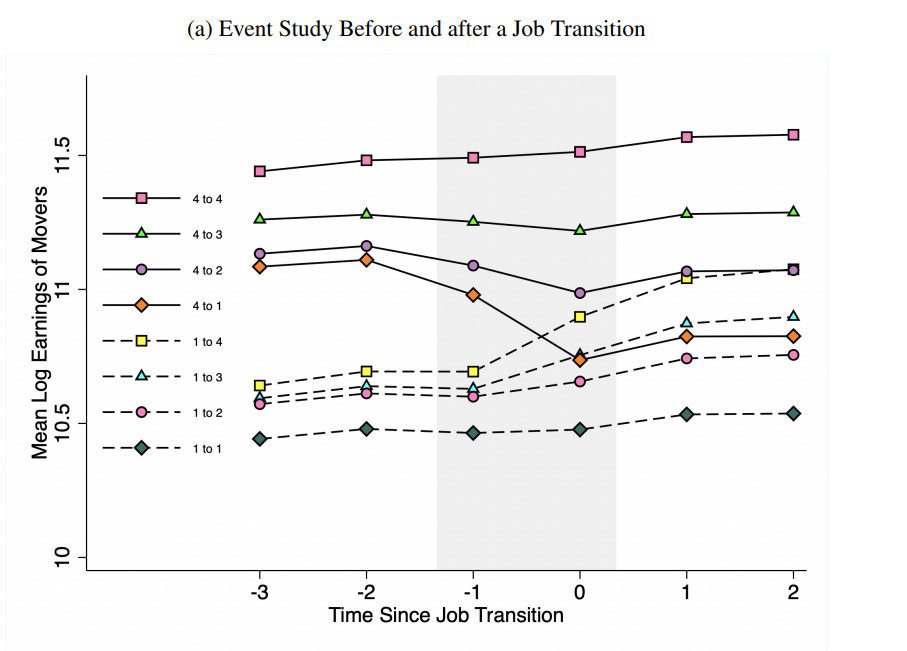

The counter that BLMS have – and really, the entirety of the literature since Card, Heining, and Kline (2013) has – is pretrends around an event study, and the symmetry of moves up and down. In the figure below, people moving up or down do not appear to be responding to changes in their productivity which show up in wages before the event. (Although we still cannot rule out sudden shocks to productivity! As we saw during the inflation period after the pandemic, wages were stuck at current employer and rose mainly through switching job to job).

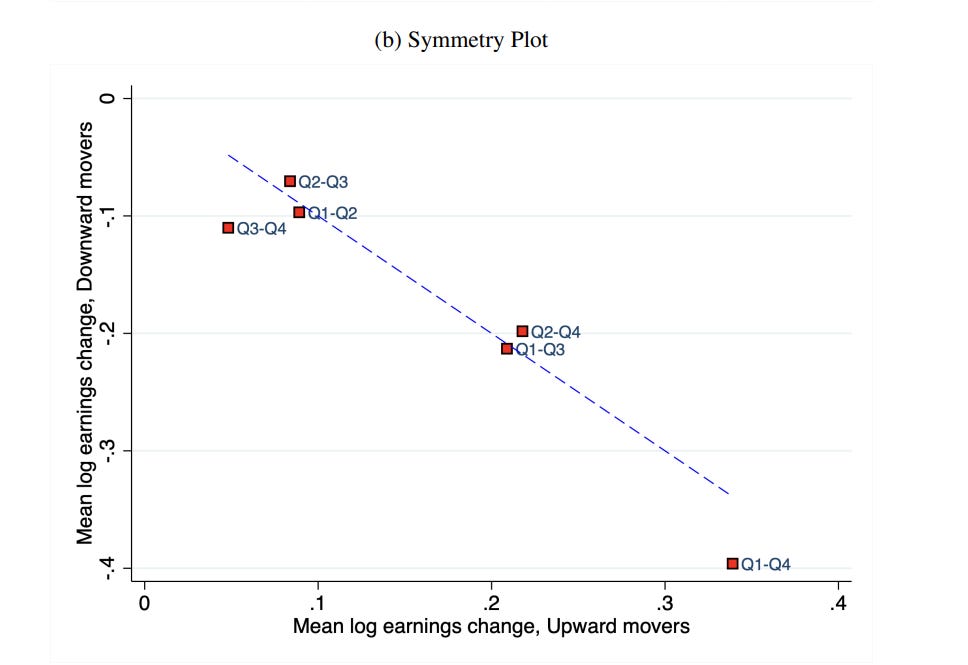

Further, the wage gains and losses from moving between different quartiles of firms are symmetric.

The deeper reason for this is that the labor market should converge to a steady state where everything balances out. Otherwise, everyone’s wage would be increasing just through searching and searching for better jobs. We can get respectable estimates of the firm wage premiums in this way. Notably, though, we cannot reliably believe the same about moves in and out of unions.

They deal with the concerns about unions affecting productivity with a sample of firms which changed unionization status, matched against counterfactual firms which were otherwise very similar. They rule out anything greater than a 5% decrease in value added per worker. Unfortunately, they do not report the local average treatment effect of changing to a unionized firm, which would be extremely important for answering whether expanding unionization actually raises wages.

The last concern for the union wage premium are threat effects. If workers and companies expect wages to rise with unionization, then companies are incentivized to buy off their workers so as to prevent unionization. This will push down the estimate of the firm wage premium. Farber, Herbst, Kuziemko, and Naidu (2021) show that unions, for instance, mainly reduce inequality through spillovers onto non-union members.

BLMS do not deal with these. This would bias their estimate of the firm wage premium down, and so they are safe ignoring it, and letting the union wage premium in their paper stand as a conservative estimate.

There is another superb working paper, Derononcourt, Gerard, Lagos, and Montialoux (2025) who explore not just the average effect, but the heterogeneity across unions. I am not going to go into it in as much detail as BLMS, in the interest of space and since the labor situation in Brazil is arguably less applicable to the United States, but it is excellent. They have broadly similar results to BLMS.

My initial headline figure is based on disbelieving the perfect exogeneity of worker moves, and believing that it biases wages up, as well as at least a substantially negative effect on productivity, combining to slightly overwhelm the bias from threat effects.

So those are the effects on worker wages. But what about the effect on the real economy? As with any question that naturally involves the development of technology and new techniques, it is quite hard to answer. The evidence gets really thin. There is one truly exceptional paper, and some other bits of suggestive evidence.

Dodini, Stansbury, and Willen (2026) have the universe of workers in Norway. Between 2002 and 2010, Norway changed the tax deduction rules for union dues, which made it cheaper to join a union, but only if the union dues were previously above the cap. This gives us differential exposure, and we can get a cleanly exogenous change in unionization.

In specifically manufacturing, productivity rose. Since DSW estimate production functions, we can exclude that this is simply employment falling while capital is fixed in the short term. Employment and output rise. However, prices rise by more than the cost of labor. The markups of firms rose. So what’s going on?

The most plausible story is this. Suppose large firms have market power over labor, and small firms don’t. Unionization is a shock to the cost of labor for all firms, one which large manufacturing firms can absorb but small ones cannot. Small firms reduce their business, increasing the market share of the large firms. In a basic model where firms are engaged in quantity competition, market shares map directly onto markups. This is supported by the response of the private sector more broadly, which find the expected decrease in productivity. So be careful in how you interpret findings of productivity from unions!

In close election designs, Frandsen (2021) finds sharp declines in employment, payroll, earnings, survival, and productivity after unionization. (Note that his productivity figure is going to be overestimated, because holding capital fixed, reducing employment increases output per worker). Similarly, Bradley, Kim, and Tian (2021) find a reduction in patenting after unionization, and Kini, Shen, Shenoy, and Subramaniam (2021) find a decline in product quality.

Considering the broader spectrum of unions, Maksimovic and Yang (2023) note that unionized plants have lower and less effective incentives. There is a long literature on the effect of good management practices – notably including “paying people for doing their job well” – and unionized plants do worse on this and productivity in general, as identified by changes in state right to work laws. Lastly, Dustmann et al (2025) gives us an example of how really badly designed collective bargaining can indeed be worse for workers – Northern and Southern Italy are practically different countries, and forcing Palermo to have the same wage rates as Milan is obviously going to be bad for Palermo.

For redistribution, the relevant thing to compare to is the same redistribution implemented through the tax system. I do not think that question is tractable at the moment. We would have to know the degree of distortion across many different markets. Nevertheless, it is difficult to believe that unions are the most efficient way.

If we want to limit the damage that a union can do, a simple means would be through limiting what unions can bargain over. Rather than only bargain over wages, unions often impose rules on how many people must be used in a production process. Numerous examples of these are given in section 2.1 of Bridgman (2015), and often include people who are required to stand around doing nothing for a job to be done. These practices are rampant in public sector construction unions, most notoriously in subway tunnel digging. By requiring someone to show up to a job at which they are completely unproductive, such rules are necessarily worse than the same amount of money simply delivered as a transfer.

Finally, there is no good case for public sector unions. There is no plausible labor market inefficiency which they are fixing. Governments are not profit maximizing entities, and are not choosing their labor quantity based on utility maximization. Public sector unions are justified only if it’s better for redistribution on the basis of marginal utility to come attached to skilled jobs which the poorest of the poor are inequipped to hold. I do not think this is the case.

First off, this was very well written. You've also successfully rage-baited me;

"Masters are always and everywhere in a sort of tacit, but constant and uniform combination, not to raise the wages of labour above their actual rate... We rarely hear, it has been said, of the combinations of masters; though frequently of those of workmen. But whoever imagines, upon this account, that masters rarely combine, is as ignorant of the world as of the subject." - Adam Smith

The IBEW was founded in 1891. Mainly because electricians were dying left & right.

Your assumptions are hilarious ngl.

Public workers have no business unionizing

That right was reserved for workers in the private sector

The end